Implementing FASB ASU on Contributed Nonfinancial Assets

In September 2020, the Financial Accounting Standards Board issued Accounting Standards Update (ASU) 2020-07 Not-For-Profit Entities (Topic 958): Presentation and Disclosures by Not-For-Profit Entities for Contributed Nonfinancial Assets. The intent of ASU 2020-07 is to provide enhanced transparency related to the presentation and disclosure of contributed nonfinancial assets. These enhancements will allow a clearer understanding of both the volume and type of nonfinancial assets that are received and recognized by an entity. Additionally, the ASU provides improved transparency into “cash versus non-cash” contributions and the impact on an organization’s operations. ASU 2020-07 does not change the historical valuation methodology used by the organization nor “how” that asset is recorded within the financial statements (only the “where”).

Adoption is required for annual reporting periods beginning after June 15, 2021. Thus, the ASU is effective for the June 30, 2022 year-ends and later. The ASU must be applied on a retrospective basis and comparative presentation is required if the organization presents comparative financial statements. Additionally, the transition disclosure requirements must include the nature and reason for the change as well as how the adoption of the ASU was applied.

Let’s take a step back however and determine what constitutes a nonfinancial asset.

Whatever was recorded previously as nonfinancial assets is now subject to the requirements of ASU 2020-07. This includes, but is not limited to, the receipt of donations of the following nonfinancial assets:

| Legal Services | Accounting services | IT Services | Pharmaceuticals | Commodities |

| Raffle items | Space | Personal protective equipment |

Radio, social media and television (streaming) advertising (PSAs) |

Travel (airline tickets, hotel nights, etc.) |

So at this point you are asking yourself, then what really changes upon adoption of ASU 2020‑07?

For most entities, there will be significant revisions to both the presentation and disclosure of nonfinancial assets. The overview below summarizes key changes for both of these areas.

Presentation

ASU 2020-07 now requires that nonfinancial assets be segregated from financial assets within all financial statements (statement of activities, statement of functional expenses, etc.). ASU 2020-07 does not mandate the disaggregated level that is required in the financial statements; however, in practice, many organizations are leaning toward multiple levels of disaggregation to ensure transparency considerations are adequately considered. For example, prior to adoption of ASU 2020-07, an organization may have presented a single line for contributions. Upon adoption of ASU 2020-07, at a minimum, the presentation would show a disaggregation into two lines labeled “contributions – financial assets” and “contributions – nonfinancial assets.” Many organizations are further disaggregating their nonfinancial asset contributions into such line items as: “contributions — donated services,” “contributions — donated equipment,” ”contributions – donated materials/commodities,” etc. as these presentations will more fully align to the required footnote presentation discussed below.

Disclosure

ASU 2020-07 requires significant enhanced disclosure(s) regarding nonfinancial assets. All of the following must be addressed by category of nonfinancial assets (see earlier discussion of consideration of groupings):

- The organization must disclose its policy on liquidating instead of using the donated nonfinancial asset(s) within the significant accounting policies (and, if the organization doesn’t currently have a policy, one needs to be developed).

- Qualitative considerations on whether the contributed nonfinancial assets were liquidated or used during the reporting period.

- If the nonfinancial assets were used, a description of how the asset was utilized by the organization is required (i.e., detail of which program or supporting service utilized the nonfinancial assets).

- If there were any donor-imposed restrictions related to how the contributed nonfinancial assets were utilized.

- Valuation techniques utilized in assessing the value of the nonfinancial asset.

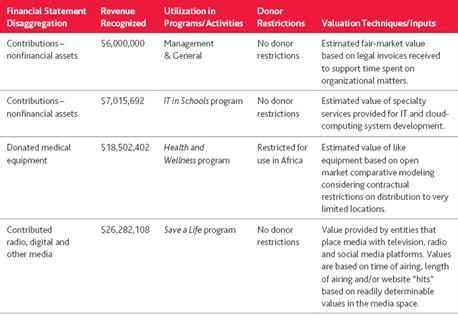

Example disclosure: The below example presents a general disclosure in a tabular format for an organization with multiple types of donated nonfinancial assets.

Implementation considerations

To date, the most important factor in successfully addressing ASU 2020-07 implementation has been ensuring a full inventory of donated nonfinancial services is available by taking a survey of the various departments of the organization. In addition, revisiting fiscal year 2021 to ensure the comparative presentation and disclosure requirements are addressed.

Furthermore, most entities are enhancing their internal policies to succinctly address the use of nonfinancial assets and “intent” from the donor regarding donated nonfinancial assets. Finally, organizations’ managements are finding the use of the tabular disclosure presentation, versus a solely narrative disclosure, provides a more transparent and informative presentation option. Many organizations feel the tabular option allows the reader of the financial statements easier access to disclosures supporting the presentation of nonfinancial assets in their financial statements.

Written by Matt Cromwell. Copyright © 2022 BDO USA, LLP. All rights reserved. www.bdo.com