OMB Issues The 2021 Compliance Supplement

By Tammy Ricciardella, CPA

On Aug. 12, 2021, the Office of Management and Budget (OMB) issued the 2021 Compliance Supplement (Supplement). The Supplement is effective for audits of fiscal years beginning after June 30, 2020. The Supplement can be accessed on the OMB website.

The Supplement is issued annually to assist auditors by providing a source of information related to various federal programs and assist with the identification of compliance requirements. However, auditees, both for-profit and nonprofit, should be familiar with the content included in the Supplement as it relates to their federal funding. The Supplement includes information related to the Provider Relief Fund, Coronavirus Relief Fund (CRF) and Education Stabilization Fund (ESF) among many others.

There are numerous changes in the Supplement this year that will be important for those with federal funding to focus on. Some highlights are as follows:

Part 2, Matrix of Compliance Requirements, is important to review to determine the programs included in the Supplement and the compliance requirements that will be subject to audit. Although auditees need to ensure they comply with all requirements of their agreements from the federal agencies and pass-through entities, the Supplement is helpful to see which compliance areas will be subjected to audit for their major programs.

Part 3, Compliance Requirements, has been updated to reflect the August 2020 Uniform Guidance revisions. In addition, the section for the reporting compliance requirement has been updated to reflect changes to the Federal Funding Accountability and Transparency Act (FFATA) that is applicable for certain major programs. Auditees should be aware of these requirements to ensure they are in compliance with the FFATA reporting.

Part 5, Student Financial Assistance, has been updated significantly to reflect numerous compliance requirement changes.

All recipients with federal funding should read Appendix V, List of Changes for the 2021 Compliance Supplement, and Appendix VII, Other Audit Advisories. Appendix V lists the changes to the programs that were made in the Supplement and Appendix VII focuses on additional guidance on COVID-19 funding and other matters. Appendix VII contains a definition of COVID-19 funding and makes it clear that only funding from one of the following federal programs that was received by an entity as a new program or funding to an existing program meets the definition of COVID-19 funding referred to throughout the Supplement:

- Coronavirus Preparedness and Response Supplemental Appropriations Act

- Families First Coronavirus Response Act

- Coronavirus Aid, Relief, and Economic Security Act (CARES Act)

- Coronavirus Response and Relief Supplemental Appropriations Act (CRRSAA)

- American Rescue Plan (ARP)

Appendix VII also outlines how to reflect donated personal protective equipment (PPE) on the Schedule of Expenditures of Federal Awards (SEFA). If an entity received donations of PPE without any compliance or reporting requirements or Assistance Listings (formerly CFDA) from donors, these should be shown at the fair market value at the time of receipt as a stand-alone footnote accompanying the SEFA. In addition, the amount of donated PPE should not be included for purposes of determining if the entity has met the threshold for a single audit.

However, if an auditee receives funds provided under an Assistance Listing, either from a federal agency directly or a pass-through entity, to purchase PPE these amounts would be included in expenditures on the SEFA.

Appendix VII reminds entities acting as a pass-through entity when awarding COVID-19 funds to subrecipients to be sure they are documenting at the time of the subaward the fact that the funds are COVID-19 funds and providing the Assistance Listing number and the dollar amount of COVID-19 funds.

Subsequent to the release of the Supplement, OMB has announced that they plan to issue two Addenda. The first Addendum is to be issued in early Fall and likely include the Coronavirus State and Local Fiscal Recovery Fund (Assistance Listing 21.027) and updates to the Education Stabilization Fund (Assistance Listing 84.425). The second Addendum is to be issued later in the Fall. The second Addendum is expected to include the following three Treasury programs: Capital Projects Fund (no Assistance Listing yet); Homeownership Assistance Fund (Assistance Listing 21.026); and the Local Assistance and Tribal Consistency Fund (no Assistance Listing yet). The second Addendum may include additional new programs.

OMB will post the Addenda to the CFO.gov website when available. The Addenda will not be posted to the OMB website; however, OMB will be responsible for reviewing the Addenda prior to issuance and they will be considered an official part of the 2021 OMB Compliance Supplement.

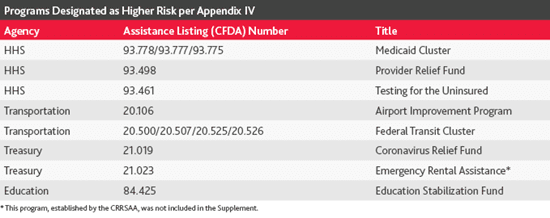

Appendix IV, Internal Reference Tables, lists all COVID-19 programs arising from the COVID-19 funding listed earlier that have been identified as “higher risk.” The designation of “higher risk” programs from the ARP have not been made yet, so stay tuned for any communication of these in the forthcoming Addenda. The Medicaid cluster continues to be designated as “higher risk” as in prior years.

The designation of these new programs as “higher risk” in the Supplement may result in additional programs being identified as major programs by your auditors in the single audit. Auditees should be aware of this effect and be prepared for this reality. This will mean that additional documentation and support may be required by the auditors.